Revenue Jersey is responsible for collection and administration of taxation revenue which funds Jersey’s public services.

Background

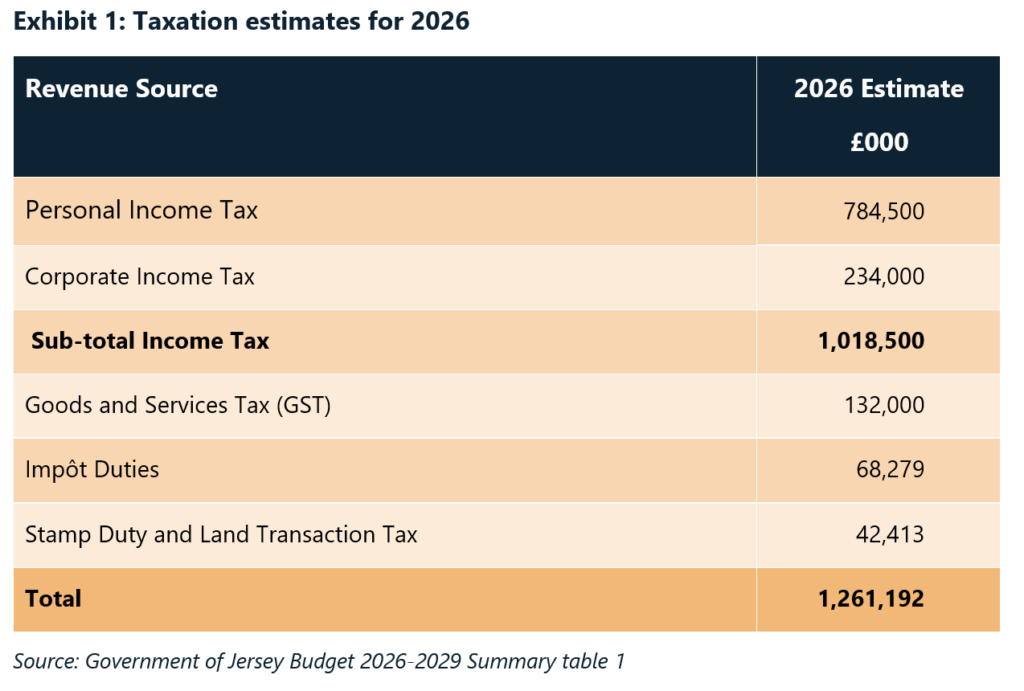

The Budget for 2026 forecasts total revenues over £1,260 million as shown in Exhibit 1. taxation revenues are shown in Exhibit 1.

Revenue Impôts are administered by the Agent of the Impôts (the Head of Jersey Customs). Stamp Duty is administered by the Judicial Greffier.

Revenue Jersey administers the other taxes and is also responsible for collecting Social Security (2026 estimate £285 million) and Long-Term Care (LTC) contributions (2026 estimate £51.6 million) as the agent for the Minister for Social Security. In addition, Revenue Jersey has a role in ensuring that Jersey’s international tax agreements are administered effectively and supports the Treasurer in forecasting income each year.

Revenue Jersey has a stated aim to be among the best of smaller tax administrations.

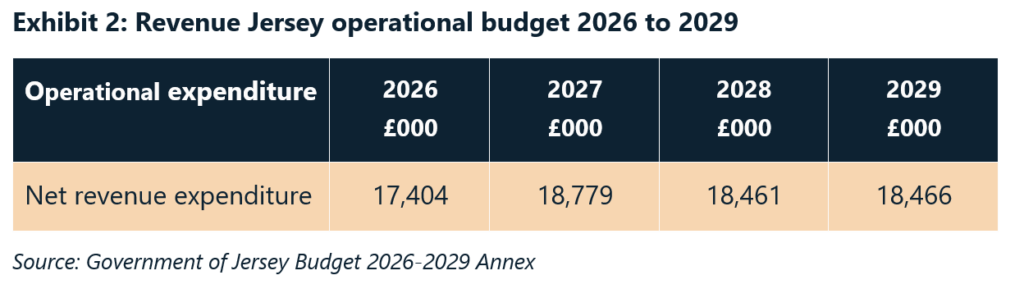

The budget estimates for Revenue Jersey for 2026 to 2029 are shown in Exhibit 2.

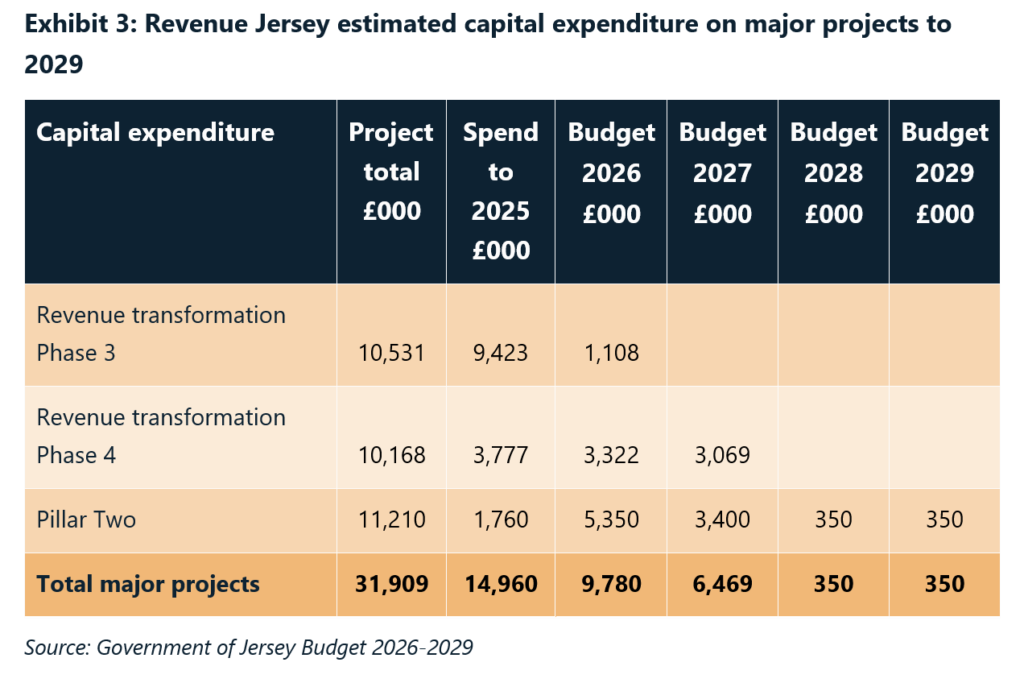

The Budget 2026 to 2029 also includes significant investment in ongoing major projects totalling almost £32 million. The expenditure forecasts are shown in Exhibit 3.

Revenue Transformation Programme

The Revenue Transformation Programme (RTP) Phases 3 and 4 are major projects that are intended to enable adaptations for digital tax systems to take account of changes in tax legislation including the adoption of independent taxation, changes in respect of the prior-year basis and the requirement for automatic exchange of tax information internationally.

Total funding of £20.7 million has been approved for these two phases which are planned for completion by the end of 2027.

Pillar 2

Jersey is implementing the Organisation for Economic Co-operation and Development’s (OECD’s) Pillar Two reforms, reinforcing its commitment to international tax cooperation and introducing a global minimum tax for large multinational enterprises. To support these reforms, the Government is investing in a new IT system, delivered in phases. This includes a secure portal for multinational groups and tax agents to register, file returns, and make payments, alongside tools for Revenue Jersey to manage new tax types, monitor compliance, and exchange data internationally.

Scope

The audit has evaluated how well Revenue Jersey uses its resources to manage risk, and to ensure it delivers an efficient, effective and economic service.

It has considered:

- leadership and governance

- performance management, including:

- information used for decision making

- prioritisation of activity; and

- value for money.

The audit covered Revenue Jersey’s business as usual activities as well as the use of growth funding for the major projects of:

- Revenue Transformation Programme (independent taxation); and

- Pillar Two implementation.

The audit did not consider tax policies and tax policy development.

Conclusions

The statutory basis for administration of taxes and other charges is set out in the Revenue Administration (Jersey) Law 2019. This Law also describes the role of the Comptroller of Revenue as the responsible officer for the collection and administration of taxes and charges.

While Revenue Jersey is part of Treasury and Exchequer, it operates independently. The Comptroller of Revenue reports periodically to the Minister and Treasurer of the States on operational performance.

The roles of the statutory officers are clearly and comprehensively described in the Revenue Jersey Governance Framework document dated November 2025 (4th review). The Governance Framework includes a range of committees, groups and other fora which are responsible for specific aspects of Revenue Jersey. The Terms of Reference for each of the main groups are also well documented in the Governance Framework document.

While the governance structure is comprehensive it involves a significant number of officers. There is an opportunity to assess the added value from each group reporting to the Executive Management Board (EMB) and consider whether any business could be consolidated into the EMB role.

Processes used by Revenue Jersey are comprehensively documented. Revenue Jersey takes the opportunity to consider consolidation and streamlining processes as part of periodic reviews of standard operating procedures.

A wide range of data is produced to enable management to monitor performance across the whole range of activities on a monthly, quarterly and annual basis.

Revenue Jersey has made significant improvements in its approach to compliance work in the last five years which has resulted in substantial benefits in the form of additional revenue and avoidance of lost revenue. Since 2022, it is estimated that additional revenue generated is over £225 million with £95 million of this being cash banked in each year following compliance interventions related to prior years of assessment.

Revenue Jersey maintains detailed records of customer feedback within the Customer Feedback Management System database. In the 12 months to March 2026, 95 complaint cases were recorded on the database with 129 associated underlying reasons for the feedback.

There is significant current investment in modernising Revenue Jersey systems and approaches. This includes progress towards independent taxation within the broader Revenue Transformation Programme, following agreement by the States Assembly in 2019, and implementation of Pillar Two. The major projects of Pillar Two implementation and Independent Taxation are both supported by comprehensive business cases and project management structures.

The States Assembly voted on amendments to independent taxation in 2023 without consideration of the increased costs of implementation. The votes were contradictory and were resolved through a further proposition in 2024. In addition to the delay, the increase in implementation costs was subsequently estimated at £347,000.

Revenue Jersey has a publicly stated ambition on its website that ‘Revenue Jersey aims to be among the best of smaller tax administrations’. While there is evidence to demonstrate improvements being made, there is limited comparative data from smaller tax administrations to benchmark progress towards the stated ambition.

The Service Performance Measures (SPMs) are published by the Government of Jersey on a quarterly and annual basis and include five performance measures attributable to Revenue Jersey. Performance for all of these measures exceeds the targets set.

The published performance data across the range of Revenue Jersey activities represents good practice. The transparency is greater than other jurisdictions reviewed during my audit.

There is evidence that Revenue Jersey uses technology to improve value for money. This includes ongoing development of automated processes and tools to manage performance and data in respect of workflow planning, compliance work, audit work, customer feedback and promoting online filing as part of the annual compliance programmes. However, there are also examples where further work is needed to demonstrate that technology is being used effectively to deliver value for money.

The percentage of personal taxpayers filing online in Jersey is low at 54% when compared to other jurisdictions. A 2024 survey by the OECD shows that the global average is over 90%. Many other jurisdictions, including smaller ones, have mandated online personal tax filing as well as corporate tax. Evidence shows that online filing can reduce costs as well as increasing yields and reducing the risk of fraud and error. Despite current filing rates, the target remains at 50%. This target is not challenging for Revenue Jersey and conflicts with its published aspiration.

Revenue Jersey also relies on postal communication with taxpayers for much of its business including making refunds by cheque. The cost of processing postal communication associated with the tax and social security base of £1,597 million is over £250,000 each year.

Conclusions

Revenue Jersey operates as an independent tax administration with its functions and key roles set out in statute. The governance structures, clear roles and responsibilities together with reporting arrangements are effective in ensuring that the integrity of the independent role is not compromised. Governance processes and systems are thoroughly and comprehensively documented and kept under review.

Where there are areas of inefficiency, these are understood but progress to improve and deliver greater efficiencies is slow due to constraints on resources and capacity. There is evidence that Revenue Jersey is inefficient due to digital immaturity which increases cost and increases risk.

Major projects on independent taxation and implementation of Pillar Two are supported by detailed business cases and project plans. Implementation is on track.