Background

It is not unusual for the delivery of major infrastructure projects to span more than one election cycle. However, it is now over thirteen years since the States Assembly required the Council of Ministers to bring forward proposals for investment in hospital services, including detailed plans for a new hospital. In that time more than £200 million has been spent on various hospital projects, including on site acquisition and preparatory infrastructure, but with no construction having yet commenced on a new acute hospital.

The New Healthcare Facilities (NHF) Programme began in 2023 with a renewed focus on proof of concept and feasibility following the review of the Our Hospital project in late 2022. The NHF Summary Strategic Outline Case (R.111/2023) and Feasibility Study (R.112/2023) were presented to the Assembly in July 2023 and were updated in December 2023.

The States Assembly approved funding for the NHF Programme as part of the Budget 2025-2028. An Outline Business Case was produced in summer of 2024 which supported funding of £710 million allocated in Budget 2025 to deliver:

- an acute facility at Overdale

- meaningful progress on the Ambulatory facilities at Kensington Place and the Health Village

- some ‘meanwhile use’ work on the Ambulatory facilities at Kensington Place and utilising some of the existing Jersey General Hospital site

- the Enid Quenault Health and Wellbeing Centre at Les Quennevais, utilised on a longer-term basis

- the delivery and continued use of the St Ewolds facility for rehabilitation services

- acquisition of further land and properties necessary to deliver the programme; and

- provision and use of decant facilities.

A blended funding solution was approved for the NHF Programme as part of the Budget 2025-2028, with £523 million sourced through borrowing. To address volatility and interest rate risks, a short to medium term strategy had already been adopted utilising a Revolving Credit Facility (RCF) of up to £300 million (with a potential extension to £500 million). This is in place until 2028 with the possibility to extend to 2030.

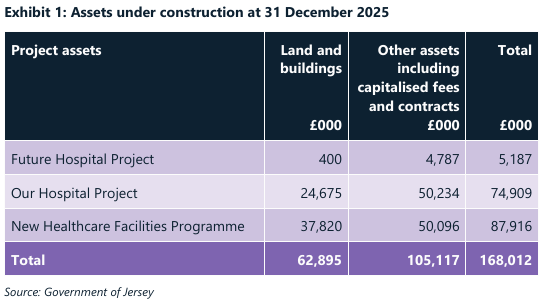

Assets under construction at 31 December 2025 include £168 million relating to the various healthcare facilities projects (Exhibit 1).

On 5 June 2026, the New Healthcare Facilities Programme announced that a contract had been signed for the Overdale acute hospital main works.

The Functions of the Comptroller and Auditor General

(C&AG)

Article 11 of the Comptroller and Auditor General (Jersey) Law 2014 requires the C&AG to:

- provide the States with independent assurance that the public finances of Jersey are being regulated, controlled, supervised and accounted for in accordance with the Public Finances (Jersey) Law 2005

- consider and report to the States on:

- the effectiveness of internal controls of the States, States funded bodiesand funds

- the economy, efficiency and effectiveness in the way the States, States funded bodies and funds use their resources; and

- the general corporate governance arrangements of the States, States funded bodies and funds; and

- make recommendations to bring about improvement where improvement is needed.

Objectives of this audit

The audit’s overall objective is to assess the extent to which the governance structure and control environment established for the New Healthcare Facilities Programme are enabling and will enable value for money to be delivered.

Scope

The audit will include all aspects of the New Healthcare Facilities Programme as well as the financing strategy for the programme.

Under the requirements of the Public Finances Manual, every Major and Strategic Project is subject to an internal audit during the life of the project and other projects may be assessed as required. My audit will consider any relevant work undertaken by the Government of Jersey Internal Audit function and will not duplicate it.

The audit will also consider any relevant work undertaken by Scrutiny Panels.

This audit will include a follow up of my Report Learning from Previous Hospital Projects: A Follow Up Review May 2023). I will also follow up on the implementation of relevant recommendations from my Report Major and Strategic Projects, including Capital Projects (November 2023).

Audit approach

This audit will use a system-oriented approach.

The audit will commence with an initial documentation request. The findings of the document review will be followed up by interviews with key officers and potentially with other stakeholders.

The audit will commence in July 2026.

The detailed work will be undertaken by affiliates engaged by the C&AG.

Audit criteria

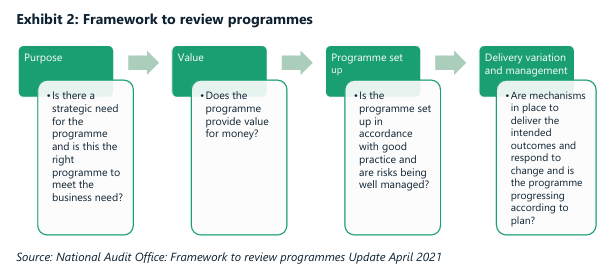

The criteria to be used for this audit are set out in Exhibit 2 and are based on elements of the Good Practice Framework developed by the UK National Audit Office.

The following criteria will be used:

- Purpose:

- Is it clear what objective the project is intended to achieve?

- Have the right people bought into the project, such as users, suppliers, those who have to implement it?

- Value:

- Do the procurement method, financing strategy and implementation option meet the programme’s objective and provide long-term value?

- Does the business case demonstrate value for money over the lifetime of the project?

- Are cost and duration estimates appropriate to the stage of development of the project, with risks and uncertainties appropriately reflected?

- Does the project have a plan to deliver benefits and is this being implemented?

- Set up:

- Are there structures (internal and external) that provide strong and effective oversight, challenge and direction in accordance with the requirements of the Public Finances Manual?

- Does the programme have the right culture and leadership with the necessary authority and influence?

- Does the Government have the resources (staffing, capability, equipment, and so on) required to support the programme?

- Are scope and business requirements realistic, understood, clearly articulated and capable of being put into practice?

- Are key risks identified, understood and addressed?

- Delivery variation and management:

- Are there appropriate incentives for all parties to deliver (contractual, performance management or other)?

- Is there an effective mechanism to control project variations?

- Is the programme sufficiently flexible to deal with external changes in the operating context?

- Are arrangements in place to measure and assess progress effectively?

- Are effective contract management arrangements in place?

- Is the programme learning from experience on previous relevant programmes and projects?