The Health Insurance Fund (HIF) provides financial benefits for medical and pharmaceutical services supplied by approved health professionals to people insured under the Health Insurance (Jersey) Law 1967.

Background

The HIF receives allocations from Social Security Class 1 and Class 2 contributions, as specified under Article 30 of the Social Security (Jersey) Law 1974. The Minister for Social Security has responsibility for the control and management of the HIF.

The benefits provided by the HIF include:

- subsidised General Practitioner (GP) consultations

- a wide range of free prescriptions at community pharmacies

- other supplies including flu vaccinations, diabetic supplies and wound dressings

- additional support to low-income families and pensioners for low fixed fee General Practice services through the Health Access Scheme; and

- free GP surgery visits for children and full time students.

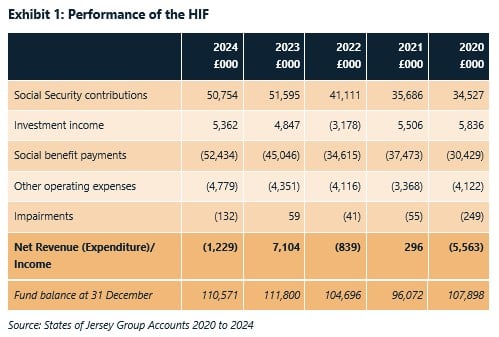

The performance of the HIF and the balance of the fund at 31 December from 2020 to 2024 are shown in

Exhibit 1.

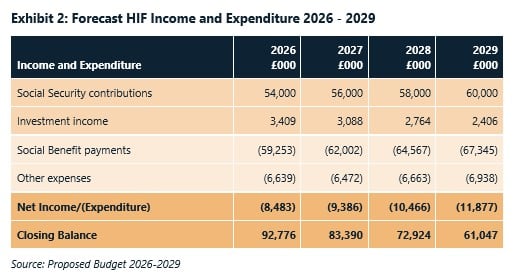

In recent years there have been a number of changes to the medical benefits funded from the HIF. As a result of these changes and other pressures on the HIF related to the ageing demographic, the forecast in the Budget 2026 – 2029 is that the HIF will show a deficit for each year of the budget period. By the end of 2029, the balance in the HIF is anticipated to be £61 million which is less than one year’s expenditure (Exhibit 2).

The Budget 2026 – 2029 states that ‘Increased expenditure against the Health Insurance Fund means that the fund will be exhausted during the early 2030’s unless action is taken soon’. This contrasts to the position reported in the Government Plan 2023 – 2027 which forecast a surplus for each year of the Plan and concluded that ‘the fund remains in good health over the medium term’.

Scope

The audit has evaluated the operation of the HIF in terms of:

- oversight and governance

- funding and investment strategy, including managing charges

- social security contributions from individuals and employers

- internal controls, including, in the context of the HIF benefits and funding:

- managing potential conflicts of interest

- avoiding fraudulent activity

- ensuring checks on compliance with HIF rules; and

- appropriate coverage of all relevant providers of primary care; and

- monitoring and reporting performance, including adherence to any funding conditions.

The audit extended to:

- those departments within Government involved with managing the HIF, namely:

- Employment, Social Security and Housing (ESSH)

- Health and Care Jersey (HCJ); and

- Treasury and Exchequer (T&E); and

- The Primary Care Body (PCB).

The audit has not evaluated the quality of health care services being funded by the HIF.

The C&AG is undertaking a separate audit of the Government’s programme of work looking at long-term sustainable healthcare funding.

Conclusions

Key findings

Overall responsibility for the HIF lies with the Minister for Social Security. However, the Minister for Treasury and Resources and the Minister for Health and Social Services also play key roles.

Monitoring of the HIF performance and activity takes place at different levels. There are however no routine Key Performance Indicators (KPIs) provided to the Minister for Social Security regarding HIF performance. In addition, there are no KPIs for HIF funded services reported in the suite of Service Performance Measures for the Employment, Social Security and Housing (ESSH) Department or Health and Care Jersey (HCJ) monthly Quality and Performance reports.

The governance arrangements for the HIF involve a number of departments and include a range of strategic, operational and working groups as well as informal groups. The relationships and interdependencies between these groups are not formally documented.

No clear plan of action has been developed for the HIF since the 2021 actuarial review despite the clear indication from the actuary that the fund is not sustainable. Instead a number of additional benefits and contracts have been funded through the HIF since 2021 causing additional pressure on the sustainability of the HIF. The current funding and expenditure model for the HIF is not sustainable without intervention. There is commitment to an overall review of the healthcare delivery model including primary care which will include consideration of the HIF.

There has been a substantial increase in funding initiatives from the HIF to support improvements in GP practices and community pharmacies in the last few years. In the period from 2022 to 2026, the additional investment available in support for general practice is estimated at £12.3 million. From 2023 to 2026, the additional investment available for pharmacies is estimated at £12.4 million.

In the same period, significant additional funding has been provided from the HIF to improve access to general practice by increasing benefits and subsidies available to all eligible patients. The annual cost of this is estimated at over £16 million.

Investment in new schemes and initiatives has resulted in ongoing improvements to the breadth of primary care services, as well as reducing the cost barrier to accessing primary care services.

The C&AG has considered the key changes made in HIF expenditure since 2023 and whether they have been supported by robust business cases. Some of these changes related to States Assembly decisions, including approved Government Plan amendments. Lynn Pamment did not observe consistency in the rigour with which business cases have been documented and did not observe good practice being adopted in some business cases supporting decisions involving significant investment.

Overall, her analysis suggests that new initiatives have been introduced without a full and consistent assessment of the long-term impact on the HIF and with insufficient consideration of resource and system implications. In addition, some initiatives lack the metrics to enable assessment of value for money following implementation.

As part of the Ministerial Decision to introduce a new contracted medical benefit of £20 in 2023, the Government agreed with all practices that price transparency would be improved. The schedule of fees charged by individual practices is now published on the website to enable patient comparisons and choice.

However, the fees published by each practice and summarised on the Government website show a number of inconsistencies related to the HIF benefit. In addition to these inconsistencies, there are also some inconsistencies in services offered which attract the HIF benefit.

While contributing a significant part of the price of routine GP appointments, the Government has no locus in influencing primary care fees. There is no control to prevent general practices from increasing fees to neutralise the impact of increased benefits approved by the Minister for Social Security. The C&AG has identified instances of fees being increased in excess of inflation in the period from February 2024 to July 2025.

Changes to the benefits paid from the HIF have added complexities to the supporting systems, which have limitations. There is an inherent risk of errors and irregularities for practices and the Government in the current systems and processes.

Conclusion

There have been significant changes to expenditure funded from the HIF in recent years. These changes have removed some cost barriers to accessing aspects of primary care and funded improvements to the breadth of services offered by general practices and community pharmacies. This includes an emphasis on prevention and quality to benefit Islanders and ease pressure in other parts of the health sector.

However, the HIF is not sustainable in its present form and there is no tangible plan for primary care in the context of a sustainable, integrated health care model for the future. The Government does not routinely assess value for money from new initiatives funded from the HIF and the changes since 2022 have increased the risk of overpayment from error or fraud.